Market Research on Meditation & Mindfulness Apps

Through in-depth research into the meditation and mindfulness app market, we have uncovered the key trends, leading players, and growth opportunities that can be applied across the fast-expanding wellness technology space.

A concise market study — size, trends, competition, and outlook.

Overview

Meditation apps deliver guided meditation, breathing, and sleep content that helps reduce stress, anxiety, and insomnia. Rising stress levels, wider smartphone use, and growing mental-health awareness are driving rapid adoption. The market is highly consolidated: two players — Headspace and Calm — hold roughly 70% of global share.

Market Size & Forecast

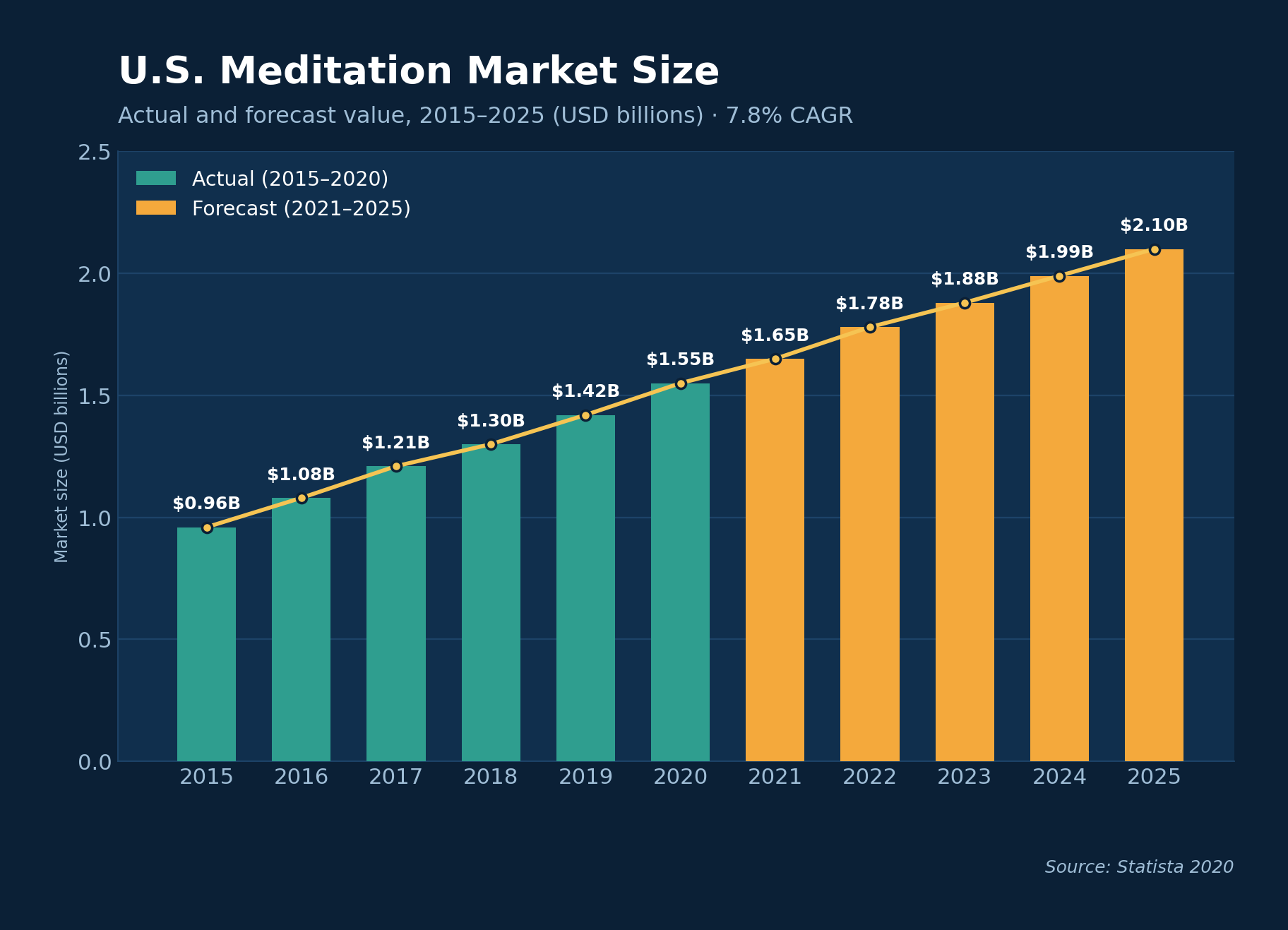

The U.S. meditation market grew from $0.96B in 2015 to $1.55B in 2020, and is forecast to reach $2.1B by 2025 — an estimated 7.8% CAGR. Steady year-on-year growth signals a maturing, expanding category.

U.S. meditation market size, 2015–2025 (USD billions). Source: Statista 2020

Key Trends

- ~52 million users downloaded the top-10 meditation apps in 2019.

- Wider smartphone and smartwatch use makes mindfulness a daily habit.

- Aging populations and rising mental-health needs expand the audience — over 53% of U.S. seniors meditate weekly.

Market Snapshot

- Market opportunity of USD 2.1B between 2020–2025 (7.8% CAGR).

- Meditation practice has tripled since 2012; ~14% of U.S. adults have tried it.

- Globally, an estimated 200–500 million people meditate.

- Headspace, Calm, and peers have seen 65M+ downloads across 180+ countries.

- North America leads today; Asia Pacific is the fastest-emerging region.

Segmentation

By operating system the market splits into iOS, Android, and others, with Android expected to grow fastest. By end-use it covers schools, offices, and personal use — the school segment is projected to lead as providers like Calm and Headspace build classroom products.

Geographical Analysis

North America holds the largest share, driven by high mental-health awareness and regular app use. Asia Pacific shows strong promise as the home of these practices, and the Middle East (GCC) remains a high-growth market for mindfulness apps.

Consumer Demand

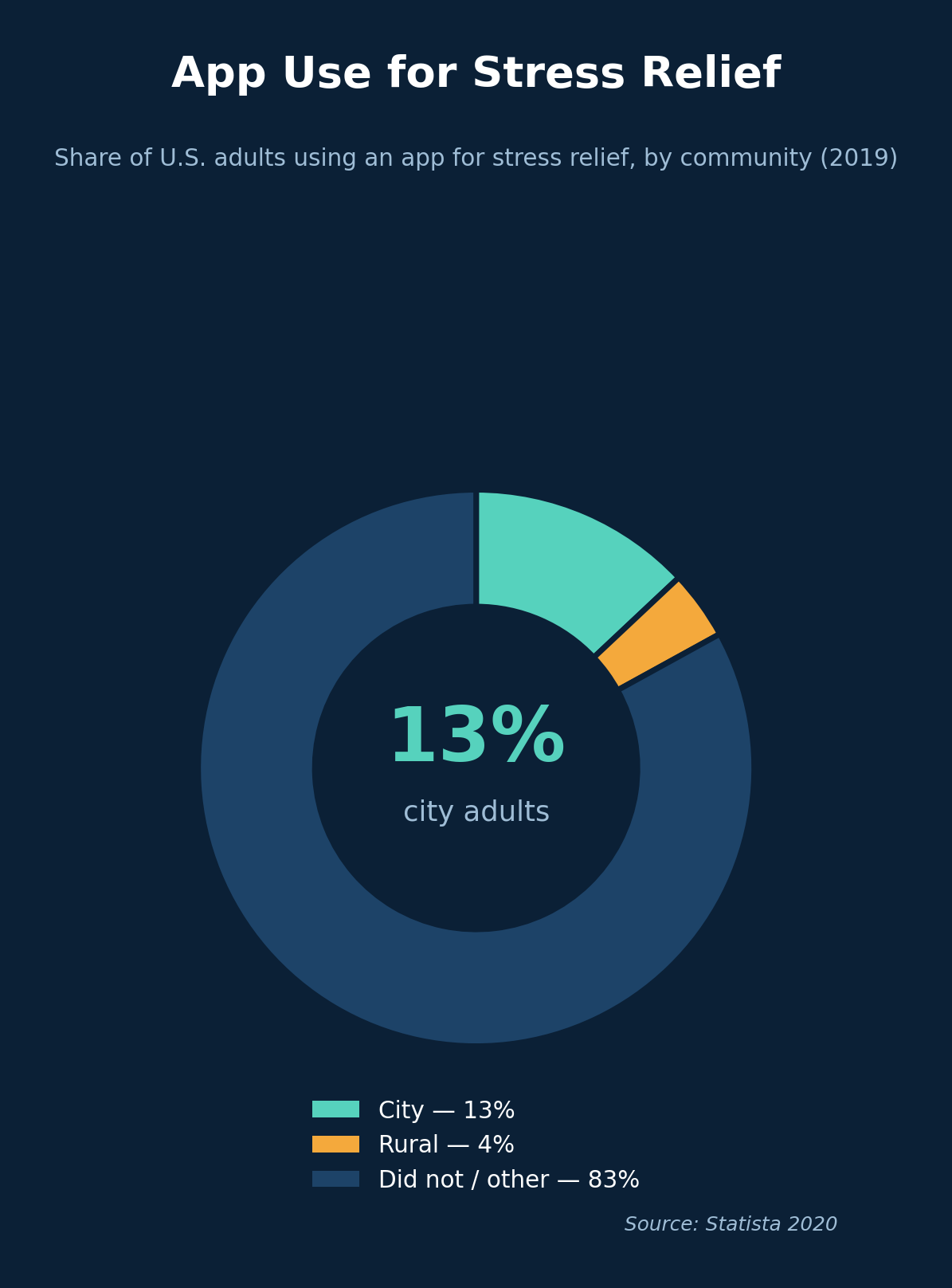

Demand is concentrated in cities: 13% of urban U.S. adults use an app for stress relief, versus just 4% of rural adults — pointing to a clear urban-first growth opportunity.

App use for stress relief, by community (2019). Source: Statista 2020

Competitive Analysis

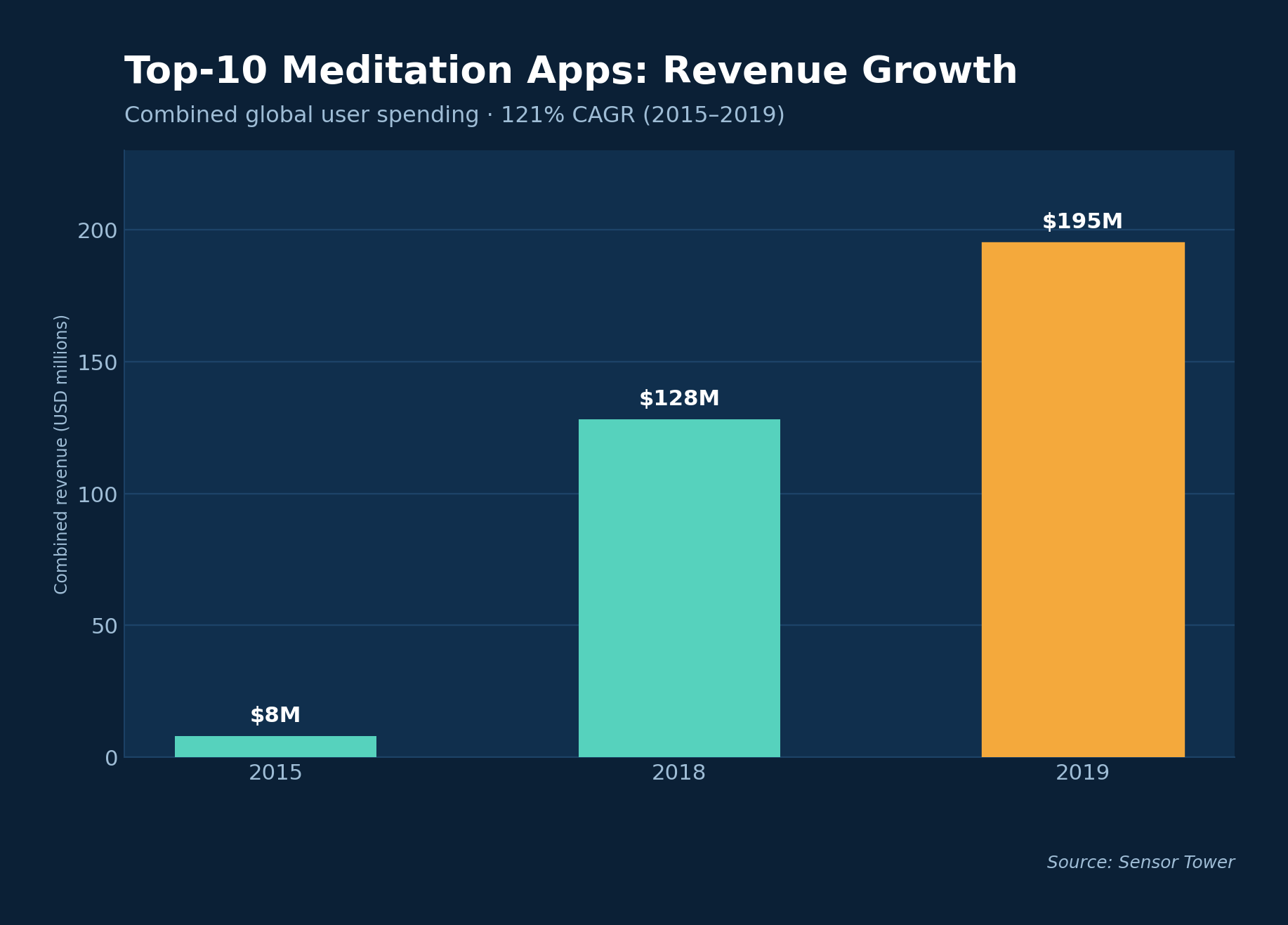

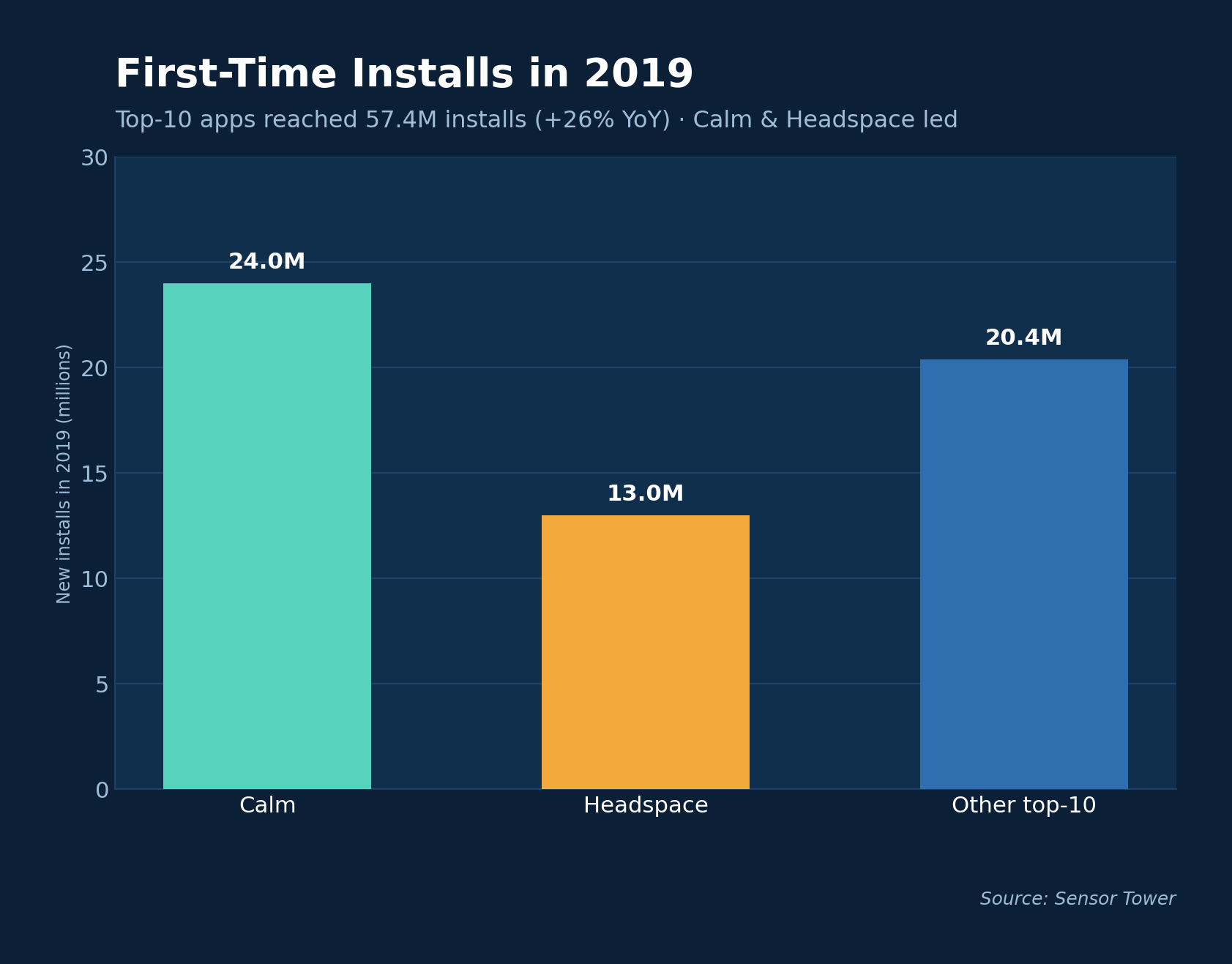

Spending in the top-10 meditation apps grew 52% year-over-year to $195M in 2019, up from ~$8M in 2015 — a 121% five-year CAGR. First-time installs reached 57.4M in 2019 (+26% YoY).

Top-10 apps: combined revenue growth, 2015–2019. Source: Sensor Tower

Calm vs Headspace: 2019 revenue and YoY growth. Source: Sensor Tower

First-time installs in 2019. Source: Sensor Tower

Market Leaders

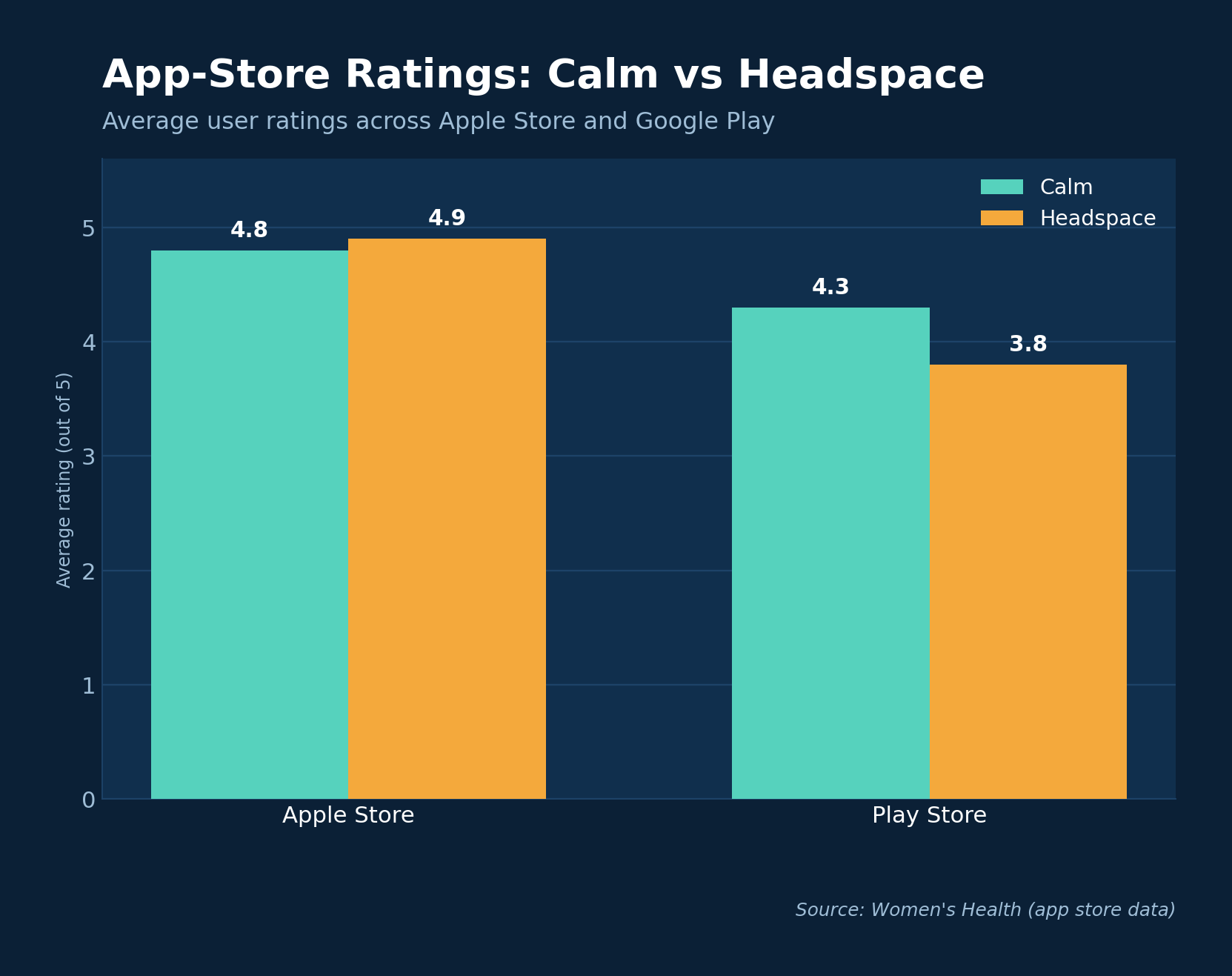

Calm and Headspace dominate on revenue, installs, and brand strength. Both score highly with users across app stores, reinforcing their lead and high switching barriers for newcomers.

App-store ratings: Calm vs Headspace.

Product Differentiation

Leading apps differentiate by content depth and niche. Headspace centers structured courses, focus music, and movement; Calm leads in sleep stories and celebrity narration; Insight Timer offers the largest free library; FitMind leans on science-backed ‘mental fitness’; and Muse adds EEG biofeedback hardware.

SWOT Summary

| Strengths • Strong, growing demand • Clear category leaders & loyal users | Weaknesses • Highly consolidated market • Heavy reliance on subscriptions |

| Opportunities • Asia Pacific & Middle East growth • Schools, workplaces, wearables | Threats • Low barriers → many new entrants • Free alternatives pressure pricing |

COVID-19 Impact

The pandemic accelerated demand as stress, isolation, and remote work pushed more people toward digital mental-wellness tools — strengthening the long-term growth case for meditation apps.

Conclusion

The meditation app market is growing steadily toward $2.1B by 2025, led by Calm and Headspace. The strongest opportunities lie in emerging regions, schools and workplaces, and wearable integration — within a competitive, subscription-driven landscape.